The United States dairy industry reported ups and downs in exports to the world over the last five years. Market Inside data shows in 2024, US exports of dairy products totaled USD 6,762 million, marginally increased from USD 6,661 billion recorded in 2023. What are the demand and supply factors to create conditions that foster or discourage U.S. dairy exports in 2025? This article will give you the answer.

Global trade is always surrounded by positives and negatives developed by market situations. 2025 will not left behind as the year has already started with a hike in U.S. tariffs. Here are five critical dairy export developments to follow in 2025.

Will China again import dairy products from the US?

While all dairy suppliers would like to see China start importing dairy products from the United States. The outlook for 2025 is clouded with contradictory signals. The current state of China’s dairy farm industry does provide some potential tailwinds to import demand given that Chinese farmgate milk prices have declined.

China recorded a decline in the production of milk by 7% in 2024 as compared to the previous year. While slower milk production may encourage stabilization within China, a broader import revival remains contingent on other key factors, most notably the country’s economy rebounding.

China’s economy continues to be challenged on multiple fronts: potential fallout from trade battles with the U.S., disappointing GDP growth, deflation, underfunded local governments, elevated youth unemployment, and real estate crisis. Economic worries are one reason consumers have clamped down on spending, and dairy consumption has been one of the causalities.

If the Chinese government’s efforts fall flat and dairy demand fails to rebound, not only will it impact U.S. shipments to that country, it will also heighten U.S. competition around the world by forcing New Zealand and Australia to target prime U.S. dairy export markets.

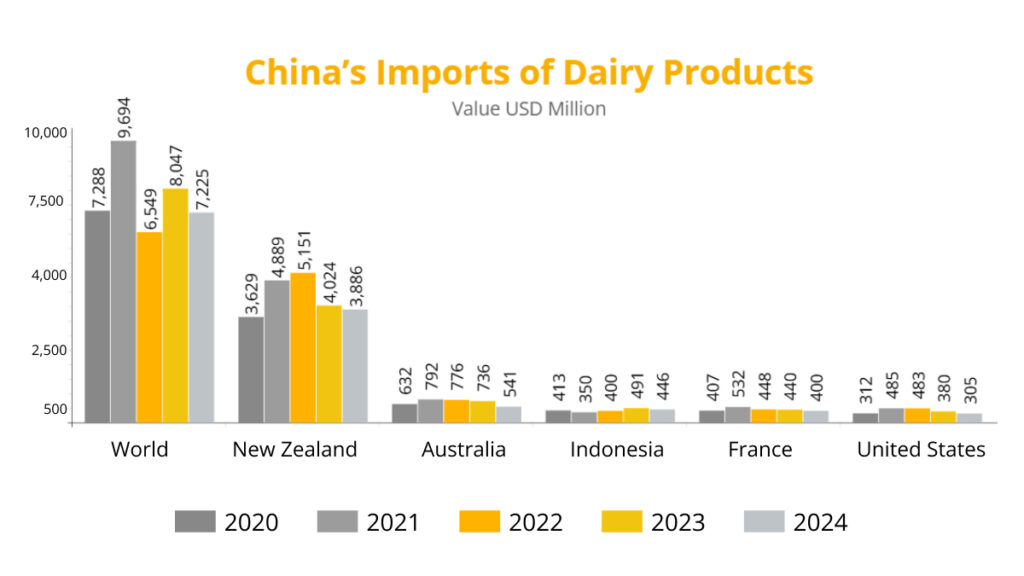

China’s total value of dairy import shipments declined in 2024 as compared to the previous year. From all import sources– New Zealand, Australia, Indonesia, France, and the United States; China diary imports fell in 2024. Look at the chart to understand China’s import market of dairy products.

| China Diary Imports | 2020 | 2021 | 2022 | 2023 | 2024 |

| World | 7,288 | 9,694 | 6,549 | 8,047 | 7,225 |

| New Zealand | 3,629 | 4,889 | 5,151 | 4,024 | 3,886 |

| Australia | 632 | 792 | 776 | 736 | 541 |

| Indonesia | 413 | 350 | 400 | 491 | 446 |

| France | 407 | 532 | 448 | 440 | 400 |

| United States | 312 | 485 | 483 | 380 | 305 |

******Value USD Million

Will Mexico continue to import dairy products from the US?

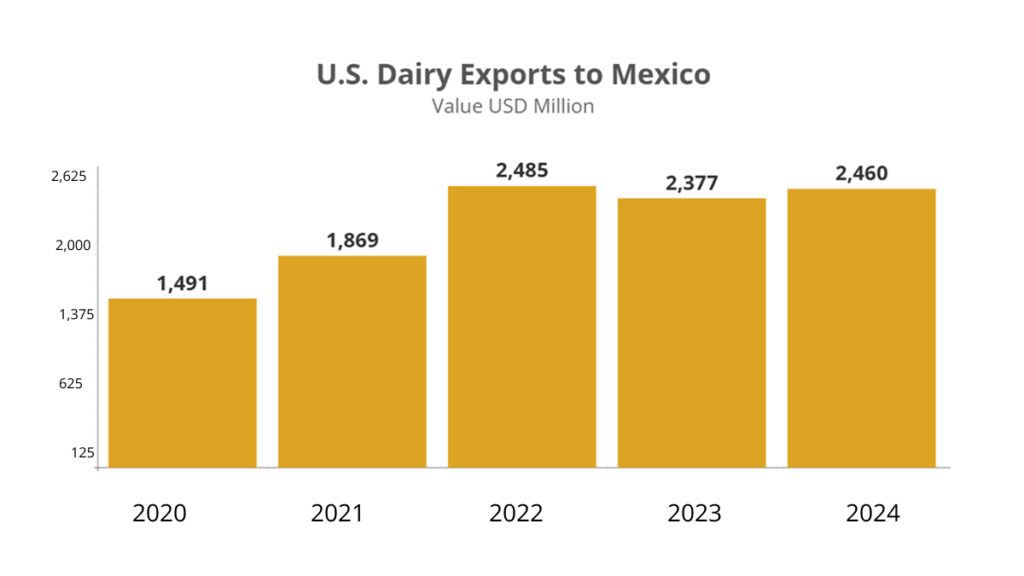

US dairy exports to Mexico reported an increase in the value of shipments for the 5th consecutive year in 2024. Mexico garnered particular attention as shipments across the southern border of the U.S. soared to record-high levels, spurred on by relentlessly strong cheese exports. The U.S. Dairy Export Council data shows Mexico’s booming demand, growing by nearly 45,000 MT in 2024, has been a welcome development for the U.S. dairy sector, especially given the fact that U.S. domestic sales declined last year by roughly 25,000 MT.

| Year | Value USD Million |

| 2020 | 1,491 |

| 2021 | 1,869 |

| 2022 | 2,485 |

| 2023 | 2,377 |

| 2024 | 2,460 |

With the formation of the Donald Trump government in the United States and the decision to hike tariffs, the question for 2025 is whether Mexico would continue to import dairy products in that way.

Will the global economy improve in 2025?

Looking beyond China and Latin America, global demand elsewhere is likely to be heavily influenced by the global economic environment. The drawn-out, inflation-plagued recovery from the COVID-19 pandemic has weighed on global dairy demand for the past two years. And while many challenges will continue to confront U.S. dairy suppliers in 2025, slow improvements in certain key parameters could bolster overall demand—and dairy demand as diets continue to shift toward more and higher quality protein.

The International Monetary Fund expects inflation to slide to 4.3% in 2025, still higher than the 3.4% average seen from 2009-2020 but another important step down from the 2022 high of 8.6%. However, inflation remains stickier for lower and middle-income countries and is likely to continue undermining the purchasing power of consumers in major markets like Brazil, Vietnam, Egypt, India, and a large portion of Sub-Saharan Africa.

In addition, GDP growth is projected to be steady to higher on a global basis, with improvements expected for key U.S. dairy buyers like Mexico, Central Americ, and the Middle East-North Africa. The growth could be amplified if countries like China can successfully navigate their delayed post-pandemic soft landings. Additionally, the ceasefire deal in the Middle East and the expected reopening of Red Sea shipping routes should benefit dairy and the general economy around the world.

Unfortunately for exporters, the U.S. dollar is expected to continue to strengthen in 2025, making imports more expensive for international consumers. Transportation costs also increased at the end of 2024, though this was partially caused by a surge in pull-forward import demand before the new year. While a higher U.S. dollar relative to other currencies and higher transport costs will create headwinds for expanding exports to Southeast Asia and other global growth destinations, those factors are unlikely to be so insurmountable as to slow the positive fundamentals within the market.

Overall, global conditions are improving as we turn the calendar to 2025 despite headwinds from high inflation baselines. Both consumers and U.S. dairy exporters should be cautiously optimistic about 2025 while acknowledging that demand is unlikely to boom and real downside risks remain.

How strong will Southeast Asia’s dairy appetite be in 2025?

While supply and demand factors continue to paint Southeast Asia (SEA) as a solid long-term driver for international dairy imports, the region’s degree of growth in 2025 and how much volume U.S. suppliers will be able to capture depend on factors like regional economic performance and Chinese demand.

SEA economic growth is forecast at 4.7%—slightly up from 2024—and inflation should continue to ease. In addition, China’s dairy imports finished 2024 on a high note and could preoccupy more of New Zealand’s milk supply in the months ahead.

Will U.S. milk production rebound?

Finally, underpinning the entire conversation is whether the U.S. will have significant exportable supplies given the limited milk production growth for much of the last two years. As we look ahead, we anticipate 2025 to be a rebound year for U.S. milk output, with growth incentives likely to outweigh the hurdles pushing back on expansion.

Looking to 2025, margins are expected to remain positive for dairy farmers, with the average DMC milk margin over feed costs for the year forecast above $14/cwt based on current futures markets. Strong profitability will undoubtedly bring new milk online throughout the country and not just around new plants. But given the tight supply of heifers due to the rise in beef-on-dairy, the speed of the expansion is the primary question.

Regardless, of whether China contracts further, stabilizes, or rebounds will certainly have a significant influence on U.S. dairy exports and prices. All told, with a rebound in U.S. milk production and a global market that is finding its footing again after several years of economic turbulence, U.S. dairy exports are poised to succeed in 2025 even as downside risks remain. Keep following Market Inside and access crucial global trade data for all the latest and complete trade updates.